The Myth of Stress Testing

Stress Testing

Many of us are familiar with mortgage stress tests in Hong Kong. It is a kind of stress testing which looks at several factors, primarily whether a borrower can meet the monthly repayments of their mortgage and all other necessary budgeted expenditures if mortgage interest rates were to increase by a certain amount.

Mortgage stress tests are only one of the many varieties of stress testing tools. In simple words, stress testing is a practical technique to assess potential vulnerability from dimensions like profitability, solvency and liquidity of an organisation or person by taking into consideration various risk factors at different stress scenarios and severities.

Stress testing is a very useful tool in the realm of risk management and is much more complex than we think it is. Some of its key components will be elaborated below.

1. Stress Scenario

Depending on the stress scenarios, the impact of stress testing can be very different. A market-wide scenario and a firm-specific scenario produce different outcomes. For instance, a market-wide scenario, say, an Asian bond market crash, compared to a firm-specific scenario, like a particular bond issuer defaulting in Hong Kong, will likely have totally different implications for the investment portfolio of an organisation.

The stress scenarios can be generated hypothetically or with reference to historical crises or events. An advantage of drawing on a historical crisis is that the stress scenarios are seen as more practical, given that it did happen before. It provides a good reference from the historical perspective. On the other hand, hypothetical stress scenarios can be more forward-looking and can cover situations where “the past does not necessarily predict the future”. It provides a higher degree of freedom by the risk manager or senior management of the organisation to incorporate more unique and adaptable scenarios to fit the nature and characteristics of the organisation.

2. Stress Severity

Stress severity, which refers to the extent of potential changes of stressed risk factors or parameters, normally ranges from high, medium to low. The higher the severity, the larger the expected change of the magnitude on the stress parameters. The wide spectrum of the severities can allow an organisation to identify its own vulnerability arising from mild to very extreme changes of risk factors. Take mortgage interest rate stress testing as an example. A mortgage interest rate parameter can be Hong Kong Interbank Offered Rate (HIBOR). A high, medium and low severity of interest rate shifting can be represented by 5%, 3% and 1% respectively for illustration. The higher the severity, the stronger the potential impact to the final stress testing results in a one stress factor model with a non-inverse relationship.

3. Risk Types

Stress testing applies to different risk types and there are a few common types of risks in risk management including but not limited to credit risk, market risk (in the trading book), operation risk, liquidity risk, interest rate risk (in the banking book), strategic risk, and reputational risk.

Market Risk – Value at risk (VAR) is a common risk measurement and stressed VAR can be one of the risk measurements to reflect the stressed market risk on the trading portfolio.

Credit Risk – The probability of default of an obligor is usually one of the key risk parameters when it comes to stress testing. The expected credit loss can be calculated by evaluating the potential loss at stress conditions with reference to a higher stressed probability of default, loss given default and the corresponding credit risk exposure. A probability of default (PD) model can be very complex but, in short, uses multivariate analysis and examines different risk characteristics of the obligor, and incorporates lots of important business attributes and relationships including but not limited to financial data, economic data and adjustments.

Liquidity Risk - One typical liquidity risk that is focused on in stress testing is the evaluation of the minimum survival period under stress conditions. Given that liquidity risk usually relates to second-round effects of other main risks, it is more complicated than single risk types of stress testing.

Take liquidity stress testing of a company as an example. Liquidity risk can result from the following main risks

i. Increase in credit risk of debtors which results in reduced cash inflow from debtors due to delinquency

ii. Increase in market risk of the trading portfolio which results in increased cash outflow associated with Mark-to-market (MTM) losses settlement and collateral posting

iii. Increase in operational risk in business contract execution with vendor & supplies, which results in settlement losses at contract execution

iv. Increase in interest rate risk arising from a rise in interest rates, which leads to revaluation losses and the liquidity cushion value being significantly affected due to interest rate curves shifts.

To maintain internal target level of liquidity cushion, additional purchase of high quality liquid asset is required, resulting in further cash outflow.

Reverse Stress Test

Normal stress tests start with considering various risk factors and translating them into a stress testing outcome through a series of calculations in different stressed scenarios. However, there is another kind of stress test called reverse stress test which works in the opposite direction. Reverse stress test starts from a known stress testing outcome and derive backwards what potential risk events can give rise to such outcomes.

Take the normal stress testing example we mentioned above. The market risk factors (increase in price volatility of the trading market) and credit risk factors (increase in credit risk of debtors) can lead to a reduction in liquidity as a stressed outcome for an organisation. Assuming the net cash flow of the company is reduced by 10% as part of the stressed outcome. Through reverse stress testing, a reputational risk event (other thank market and credit risk events) can also lead to such stress outcome. This, however, is not what the organisation would be able to think of in the first place. The organisation may normally think of market risk and credit risk as their most significant and common risk events, and not considered reputational risk factors in its normal stress testing calculation.

Nevertheless, reputation risk events, for instance, a lawsuit stemming from a customer’s complaint, could cause an organisation to have significant risks, such as additional costs in handling those lawsuits. This shows how useful reverse stress testing is in allowing organisations to identify scenarios or factors that go beyond the normal business settings and a more comprehensive set of risk events which are associated with contagion risks.

Risk Management Continuum

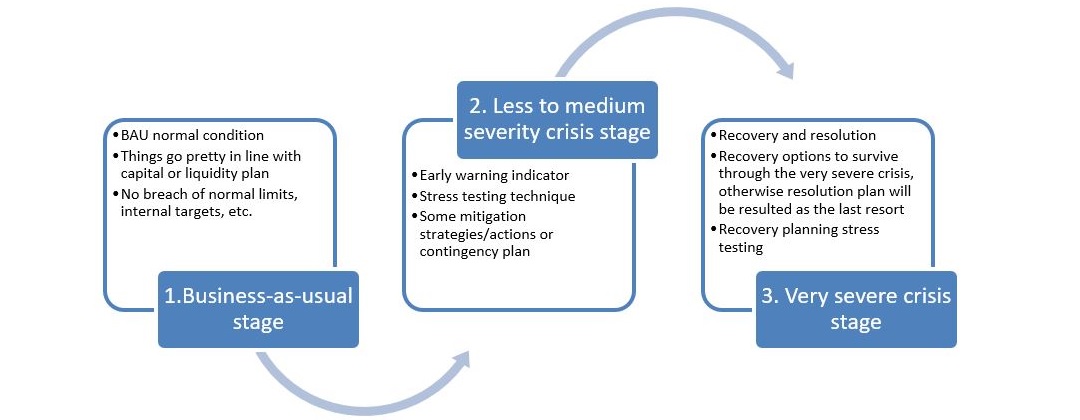

Where does the stress testing fit in across the risk management continuum?

The risk management continuum can be presented into three main stages, namely, business-as-usual stage, less to medium severity crisis stage and very severe crisis stage.

In the business-as-usual stage, there is no significant risk and business continues in line with the capital and liquidity plan. There is no breach of normal risk management limits or internal target, etc.

Nonetheless, some small to medium severity crises will happen sooner or later and these crisis events can be slow-moving or fast-moving. The fast-moving ones in particular usually can give rise to urgent liquidity needs. Through early warning indicator monitoring, the organisation has more time to make use of their liquidity contingency funding plans to mitigate the impact the crisis brings to the organisation. For those which employ a good stress testing tool and analysis on a regular basis, they should have good self-evaluation regarding potential losses arising from different stress scenarios based on the organisation’s risk profile and nature, and should already have prepared a set of risk management strategies and/or contingency plan to prepare for such potential crisis events. This will allow the organisation to survive these low to medium severity crises and return to the business-as-usual stage.

At the very severe crisis stage, a normal contingency plan does not work as it would not sufficiently compensate the huge loss or impact incurred to the organisation. More comprehensive and powerful recovery options would be needed at this stage and recovery planning stress testing would allow an organisation to better equip itself in identifying its potential vulnerability and coming up with a corresponding mitigating plan needed (i.e. proper recovery options) for this type of very severe crisis.

Application

Across the risk management continuum, stress testing is one of the key risk management pillars. It alerts an organisation to the mild to adverse unexpected outcomes related to a range of risks to which the organisation is exposed, and informs what mitigation actions it needs to withstand those potential stressed conditions.

More importantly, in a what-if scenario, the stress testing can provide a high level estimation of the tail risk of a company and hence a very useful picture for the management to develop a corresponding risk monitoring framework, risk limits, risk early warning indicators and a set of remediation options, which protect the company from falling into the resolution or bankruptcy stages.

Given that the macroeconomic environment is constantly changing, the stress testing model may have its limitation on initial data used. Apart from upfront model validation, periodical review of relevant data, assumptions, scenarios, and backtesting is very important in enhancing the performance of a stress testing model.

Future Development & Evolution

The principle of stress testing is straightforward, but the corresponding calculation and prediction of future risk driver are becoming more sophisticated. For instance, stress measure calculation of value-at-risk has been enhanced with the measurement of expected shortfall, which pose enhancement to the market risk stress testing model and its associated stress data and assumptions. It is foreseeable that the algorithm and calculation of relevant stress testing will only become more complex and the performance of such models is expected to increase thanks to the state-of-the-art technology.

Another important evolution will be integrated stress testing due to the growing demand for enterprise risk management. In order to be able to articulate a truly global enterprise-wide risk management, an integrated stress testing which requires all risk areas to share the same cash-flow, valuation, stress-testing, scenarios and projections engines is necessary to provide a holistic and comparable enterprise picture instead of having each silo and disconnected pieces of risk information and vulnerability. Without common assumptions or scenarios, there is no point in aggregating the final stress testing results, and the enterprise-wide holistic picture could not be generated based on these existing disconnected risk stress testing models.

Climate risk is also one of the hot topics recently due to the regulatory push for environmental friendliness and the Paris Agreement on reducing carbon emissions. Its associated stress testing is becoming more popular. While typical stress testing considers a time horizon of 3 to 5 years (e.g. ICAAP stress testing), climate change stress testing can cover several decades, ranging from 30 to 50 years.

Finally, there is definitely no “one-size-fits-all” or a so-called “best” stress testing method. More importantly, stress testing will only be useful and meaningful for the organisation in risk management if and only if it is conducted with proper governance, within the risk management framework and capability of the organization, and has incorporated the unique nature and risk profile of the entity.

About the author

Isaac Cheng

Head of Finance, General Manager, SPDB Hong Kong

Incorporated in the People’s Republic of China with limited liability