How we set standards & contribute to international standards

The Institute is the accounting and auditing standard-setter for Hong Kong. The Institute also sets the professional ethical standards and sustainability disclosure standards for accountants in Hong Kong.

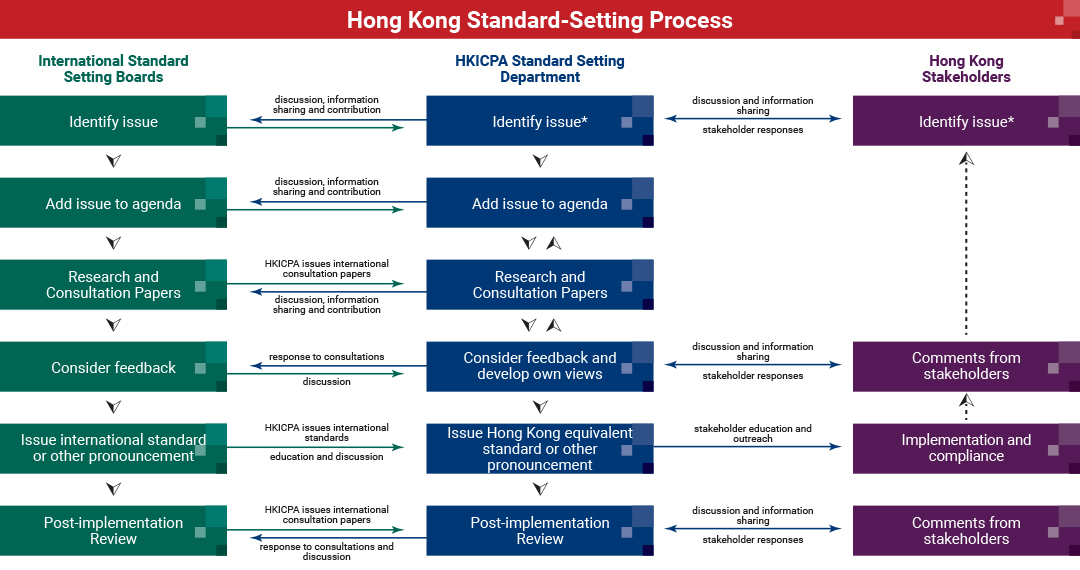

After extensive consultation on convergence, in the early 2000s, the Institute Council decided that Hong Kong standards should fully converge with international standards. Our due process documents explain our procedures for developing and adopting international standards. In summary, the process for setting standards is illustrated in the diagram below.

* Technical issues may be identified in the following manner:

If Hong Kong standards are fully converged with international standards what does the Institute do to set standards?

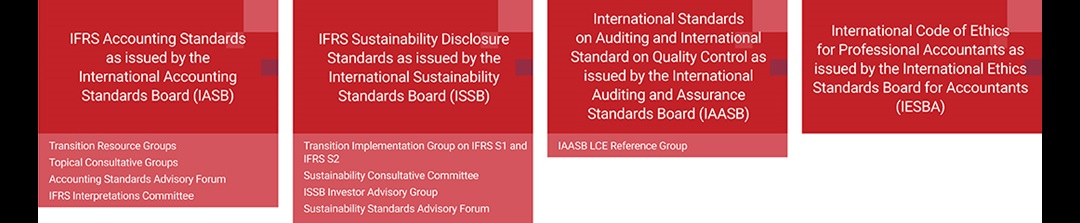

Adopting international standards that are principle-based means that the Institute has a responsibility in setting standards not just for Hong Kong but also with global markets in mind. With Hong Kong as the primary focus, the Institute voices its stakeholders' issues or concerns and reports inconsistencies in the market to international and national standard-setters; we then work together to address those matters and ensure we maintain one global set of principle-based standards that is appropriate for all IFRS jurisdictions. The diagram below outlines examples of what the Institute does to contribute to the development of international standards.

The Institute also works in collaboration with other national and regional standard-setters. The diagram below shows how we work with other standard-setting bodies globally.

- HKICPA conducts local research and outreach—the findings of which are shared with the Boards and contribute to their ongoing projects. Research or a fact-finding exercise assist HKICPA in better understanding the root cause of issues or inconsistencies, assessing the reasonableness of the matter (including whether it could be addressed through existing literature) and, to the extent feasible, recommending possible solutions to address the matter.

- HKICPA responds to key projects that matter most to our stakeholders throughout the project life cycle.

- HKICPA actively participates in and presents key topics at standard-setting meetings hosted by the Boards, including the IFRS Foundation's World Standard Setters conference, the IASB's Accounting Standards Advisory Forum (as a technical leader of the Asian-Oceanian Standard-Setters Group), and the IAASB and IESBA's National Standard Setters Meeting.

- HKICPA collaborates and discusses issues with staff of the IASB, the IFRS Interpretations Committee, the ISSB, the IAASB and the IESBA, and shares information about the Hong Kong accounting and auditing practices.

- HKICPA identifies suitable Hong Kong candidates for the Boards or their task forces and advisory groups, and provides them technical support throughout their terms.

- HKICPA facilitates dialogues between the Boards and the stakeholders in Hong Kong.

Click here for more information about AOSSG.

Click here for the IFASS Charter.

Click here for more information about the IAASB Jurisdictional & National Auditing Standards Setters Group.

Click here for more information about the IESBA National Standard Setters Group.

Click here for more information about how the IFRS Foundation works with national standard-setters.

Standard Setting Department reviews and updates (if necessary) the policy documents describing the processes in setting the Financial Reporting Standards, the Sustainability Disclosure Standards, the Standards of Professional Ethics, and Auditing and Assurance Practices (collectively “professional standards”) on an annual basis.